This section explains the classification of taxes on various financial instruments.

Comprehensive taxation and separate taxation

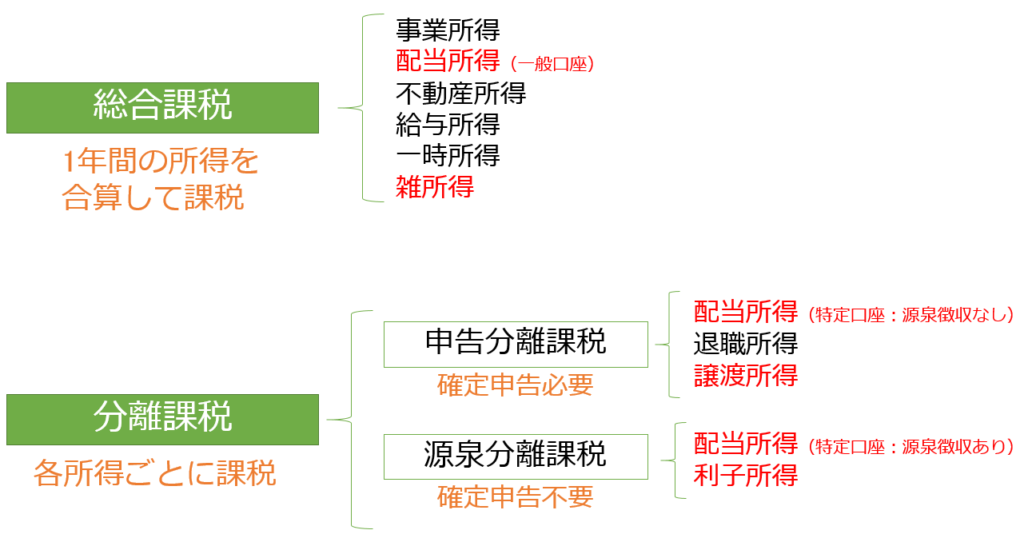

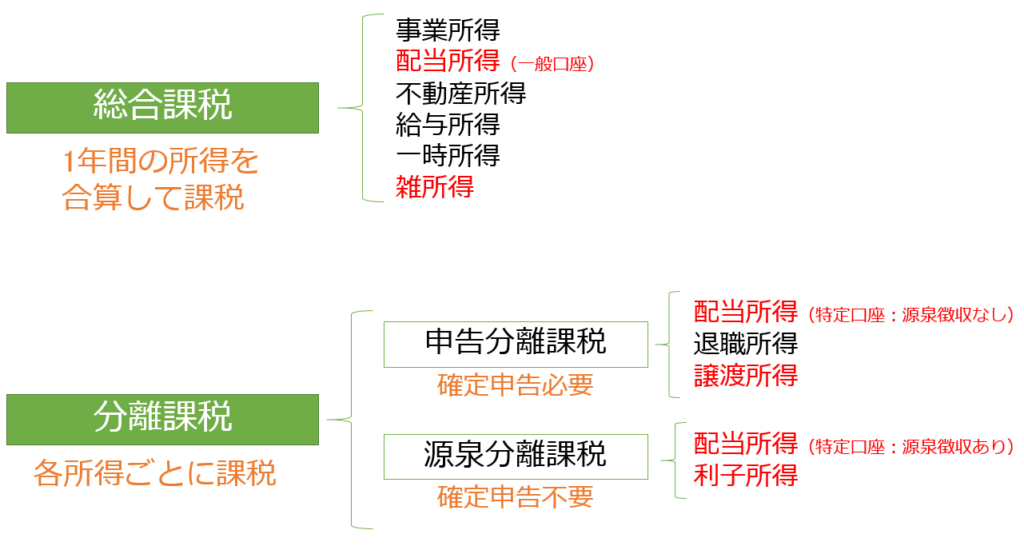

How much tax is imposed on income depends on the type of income. There are “comprehensive taxation” and “separate taxation” in the taxation method, and “separate self-assessment taxation” and “separate withholding taxation” in the separate taxation.

Comprehensive taxation is taxed by progressive taxation, which is the higher the tax rate as the amount of income is increased by combining the income covered for one year. In addition, you will need to file a final tax return depending on the amount of income.

Separate taxation is not combined with other income, but is taxed at a determined tax rate for each eligible income.

If you make everything a comprehensive tax, the tax burden will increase significantly when a large amount such as retirement income or real estate transfer income enters. The purpose of this is to reduce the tax burden in such cases.

While separate self-assessment taxation is required to file a final tax return, separate withholding taxation does not require a final return because the tax will be drawn and income will be received in the state.

In the figure above, the tax method and the type of income are shown, but the tax-related part of the financial products explained in the following is in the red.

Tax on deposits

Interest on deposits will be taxed at 20.315% at the time of payment. Income tax and reconstruction special income tax will be 15.315% and resident tax will be 5%. The taxation method is separete withholding taxation.

Foreign currency deposits

Interest on foreign currency deposits is also subject to 20.315% separate withholding tax, but care must be paid to the handling of foreign exchange gains.

If you enter into a foreign exchange futures reservation at the time of depositing foreign currency deposits, foreign exchange gains a resulting at maturity will be subject to separate withholding taxation. On the other hand, if you do not enter into a foreign exchange futures reservation at the time of depositing foreign currency deposits, the foreign exchange gain on the original portion at maturity is subject to comprehensive taxation as miscellaneous income.

Tax on bonds

The interest on the bond is the same as the interest on deposits. 20.315% tax will be charged at the time of payment. The taxation method is separate withholdingtaxation.

However, reimbursement gains on sales will be taxed separately.

Tax on stocks

The dividend of listed shares is 20.315% withholding tax. Inorder to be eligible for the dividend deduction, it is necessary to file a final tax return and be subject to comprehensive taxation.

In principle, the gain on transfer is 20.315% tax separation tax, but if you select a specific account (with withholding tax), you do not need to file a final tax return.

Tax on Investment Trusts

Stock Investment Trusts

The revenue distributions of equity investment trusts include “normal distributions,” which are portions of profit that exceed individual sources, and “special distributions,” which are portions of individual sharesthat have been refunded.

Ordinary distributions are charged 20.315% withholding tax. On the other hand, special distributions are not profitable, so there is no tax.

Public and Corporate Bond Investment Trusts

The revenue share of public and corporate bond investment trusts is 20.315% withholding tax on interest income. It is not eligible for dividend deduction.

Index-linked listed investment trusts (ETF)

Revenue distribution of index-linked listed mutual funds is withheld 20.315% as dividend income. It is subject to dividend deduction.

Real Estate Investment Trusts (REIT)

Revenue distribution of real estate investment trusts is withheld 20.315% as dividend income. It is not eligible for dividend deduction.

Summary

The following table summarizes the taxes and taxation methods for various financial instruments.

| Types of income | Taxation |

| Interest on deposits, foreign currency deposits, and bonds | Separate withholding taxation |

| Foreign exchange gains on foreign currency deposits (miscellaneous income) | Comprehensive taxation |

| Gain on redemption of bonds, gain on buying and selling | Separate self-assessment taxation |

| Dividends on stocks | Comprehensive taxation, Separate self-assessment taxation, Separate withholding taxation |

| Gain on transfer of shares | Separate self-assessment taxation |

| Ordinary distribution of stock investment trusts | Separate self-assessment taxation |

| Special distribution of stock investment trusts | They are not taxable |

| Revenue Share of Investment Trusts | Separate withholding taxation |