MMF and MRF are typical products of public and corporate bond investment trusts. I will explain what these are and what the difference is from other products.

Please refer to the following for information on what bond investment trusts are and what are the classifications of mutual funds.

Commonalities: MRF and MMF

- MRF (Money Reserve Fund)

- MMF (Money Management Fund)

Both are types of additional bond investment trusts and are operated with highly secure assets such as government bonds and local government bonds, making them very safe and highly cashable among investment trusts.

It can be purchased in units of 1 yen or more, is closed daily, and the revenue distribution is reinsinsed for one month on the last business day of each month.

As an image, it is said that the savings account provided by the securities company is MRF and the time deposit is MPF. Unlike bank deposits, the main account is not guaranteed because it is not covered by the deposit protection system.

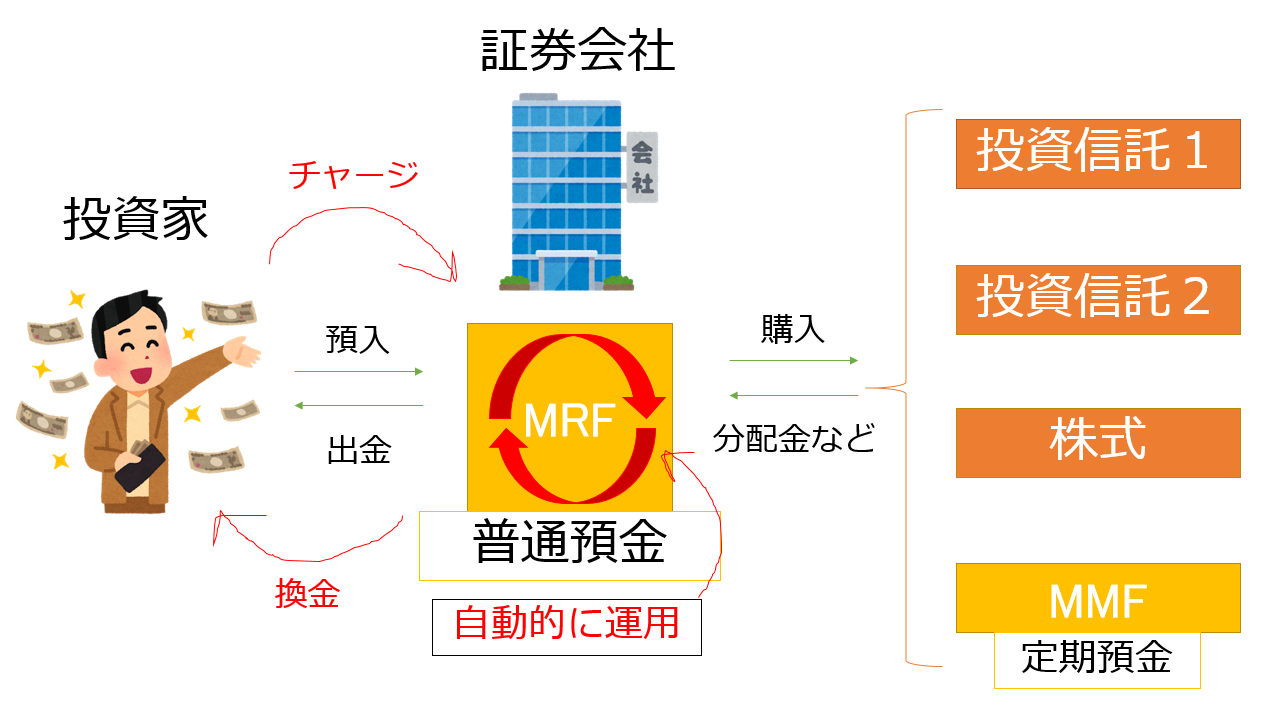

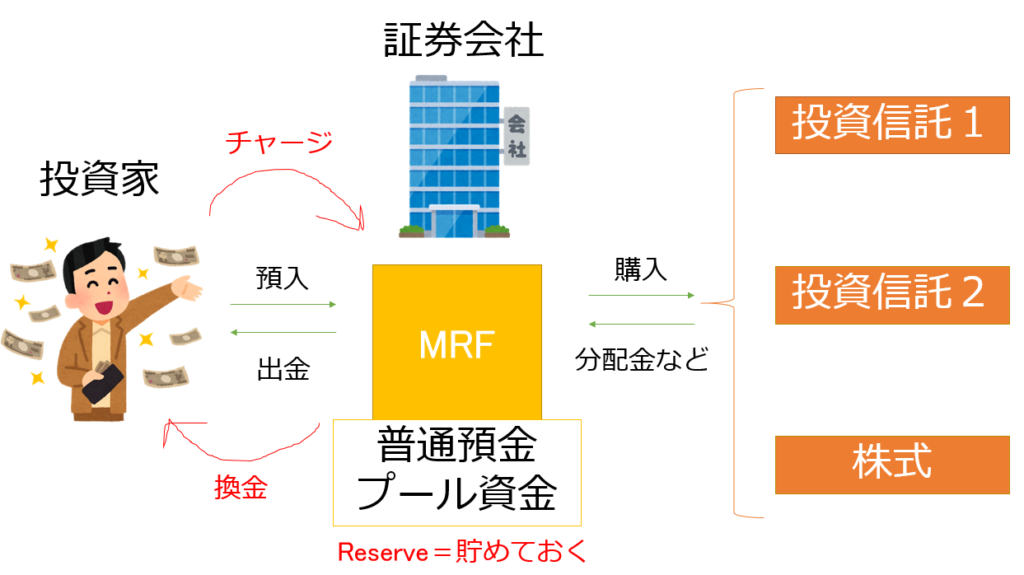

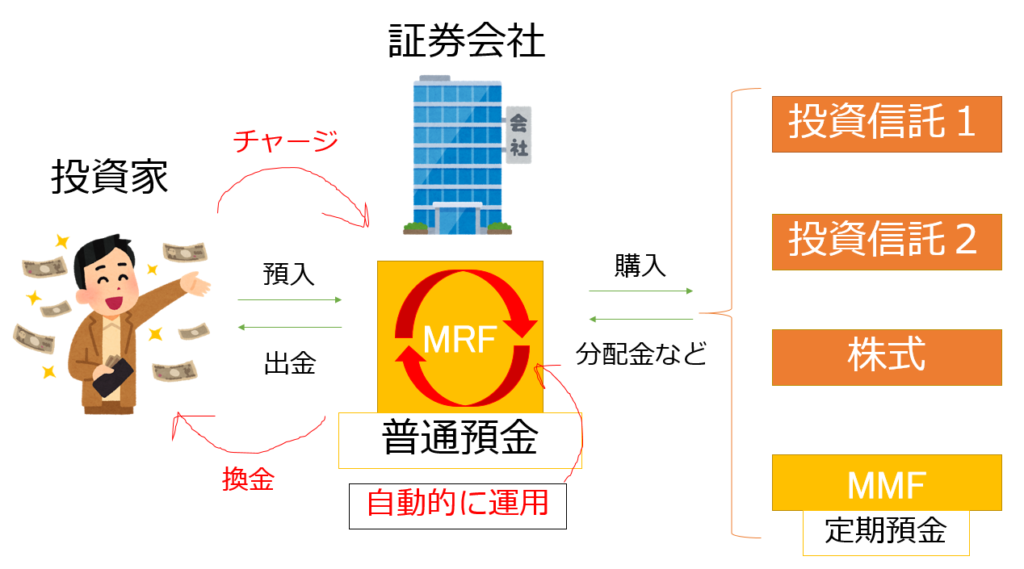

The structure of MRF

When you open an account with a securities company, MRF is also generally opened at the same time, and investment starts after the funds are transferred to the MRF. In addition, funds and distributions obtained from the sale of mutual funds and shares will be transfered to the MRF.

You can cancel at any time without penalty (trust property retention amount).

You can think of MRF as an account for keeping investment funds in securities companies, which are used to make investment procedures smoother.

As of September 2020, the annual yield of MRF at a securities company was 0.001%, and the annual yield of an ordinary bank at a bank was the same as 0.001%. Therefore, it is better to think of MRF as a regular account used by securities companies to make investments, rather than investment trusts that are used to increase assets.

The structure of MMF

The basic nature of MMF to MRF is the same as a time deposit for a bank’s savings account.

If you cancel less than 30 days after purchase, you will be charged a trust property retention amount of 10 yen per10,000 units. As a result, there is a feature that the yield is higher than MRF.

The money in the MRF is automatically operated at all time, but MMF needs to apply for a purchase each time. It is the same feeling that it does not automatically become a time deposit from the savings account though it is transferred to the savings account at the maturity of the time deposit.

Japanese yen MMF (domestic MMF) is a financial instrument that combines short-term Japanese government bonds and public and corporate bonds, but has stopped accepting purchases due to Japan’s low interest rate policy since 2016.

Similar products include stable Chinese government bond funds (China F), mainly Chinese government bonds, and foreign currency-denominated MMFs that are operated in foreign currencies such as the U.S. dollar, Australian dollar, and New Zealand dollar.

MMF denominated in foreign currency is considered to be equivalent to a foreign currency deposit in a bank deposit. As of September 2020, the interest rate on time deposits at a bank is 0.002%, the interest rate on foreign currency deposits is 0.01%, and the annualized yield of foreign currency-denominated MMF is 0.113%.

The foreign currency MMF yields look overwhelmingly better than deposit products, but it is important to note that there is no original guarantee, price fluctuation risk, and foreign exchange risk.

Summary

| Securities com pany bond investment trust | Bank | |

| Products that can be deposited and deposited at any time, and expected to be placed at a low interest rate | MRF (0.001%) | Savings (0.001%) |

| Products that yield a little better by keeping them for a certain period of time | MMF | Time deposits (0.002%) |

| Products using foreign currency with foreign exchange risk | MMF denominated in foreign currency (0.113%) | Foreign currency deposits (0.01%) |

I compared the bond investment trust provided by the securities company with the deposit provided by the bank.

Basically, the higher the interest rate (the higher the return), the greater the risk, so it is not possible to say which product is better in general. However, in the current state of ultra-low interest rates, domestic MMF and time deposits are almost the same as MRF and savings and yields, and the value of existence has been decreasing.

As I mentioned here, public and corporate bond investment trusts are very safe products compared to stocks and stock investment trusts. Therefore, in the table above, MMF denominated in foreign currencies looks like a high-risk, high-return product, but considering the overall investment from a broad perspective, it can be said that it is a relatively safe product.