In addition to commonly used bank accounts, I will explain the characteristics of various financial products such as current accounts and foreign currency-denominated financial instruments.

Ordinary Deposits

It is a deposit that can be put in and out at any time, and the interest rate fluctuates.

As of September 2020, the interest rate of a bank is 0.001%. If you deposit 100,000 yen per year, you will receive 1 yen. (This is almost no more the same level…)

Savings Deposits

As with savings accounts, it is a deposit that can be deposited in and out at any time, but it cannot be used as an account for automatic debit of utility charges or receiving salaries and pensions.

In addition, interest rates will gradually rise from 100,000 yen or more depending on the amount of deposits. However, in the current era of low interest rates, a bank has a deposit amount of 0.001% at all stages of 100,000 yen or more, 300,000 yen or more, 1 million yen or more, and 3 million yen or more.

In today’s era of low interest rates, savings and interest rates remain the same, and there is almost no value for savings deposits that cannot be set up for debits, accounts received, etc.

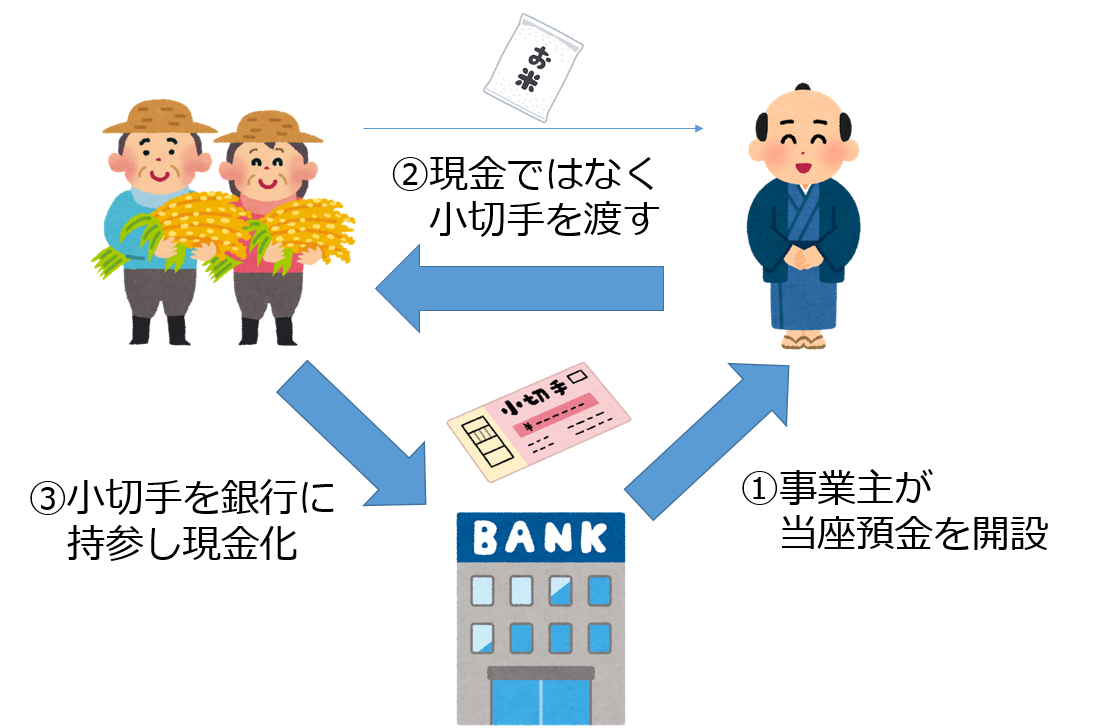

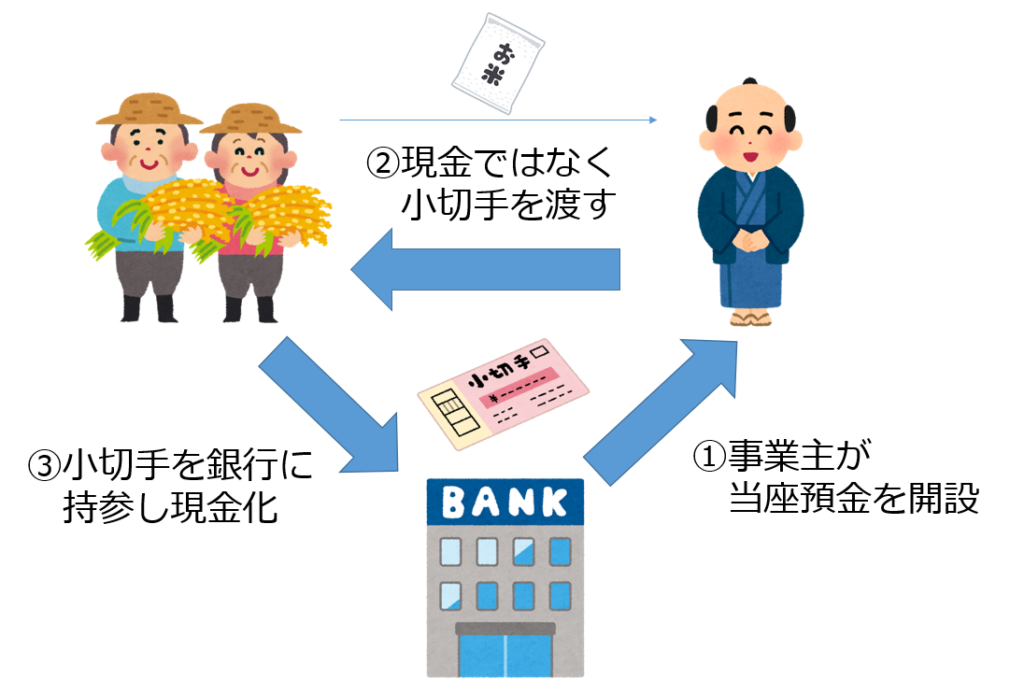

Current account

It is a deposit that can settle checks and bills, and interest is not attached, but deposits and deposits of current accounts are fully protected even if the financial institution collapses. If you have a contract called a over-the-time contract, if the balance is insufficient, you can receive the loan automatically as long as it is within the contract amount.

Current accounts are used by companies and individual businesses that trade by check or bill.

Term Deposits

I will introduce some types of term deposits, but in this era of ultra-low interest rates, interest rates are almost in common low.

As of September 2020, all regular interest rates at a bank are 0.002%. It is large when it is thought that it is twice as much as the interest rate of the ordinary account, but in this age of ultra-low interest rates, it can be said that interest income can hardly be expected because 3 million yen is deposited for one year and only 60 yen is won.

In fact, there are very few people who dare to choose time deposits now because asset management income of mutual funds and insurance can be much more expected than interest income of term deposits. For banks and other sellers, commission income, such as mutual funds, is more delicious, so the reality is that they recommend mutual funds rather than time deposits.

Super-periodic

It is a deposit that selects a period of one month to ten years and deposits a lump sum of funds during the period, and the interest rate is fixed.There is also a half-year compounding type, but only individuals with a deposit period of 3 years or more can choose.

Large-sized period

The deposit amount is a time deposit of 10 million yen or more, and the interest rate is fixed.

Due date specified period

After the one-year retention period, you can set the maturity date to any day one month before you want to cancel and cancel without penalty.

Variable interest rate period

In general, it is a term deposit that interest rates are reviewed every six months.

Japan Post Bank

Since Japan Post Bank was operated by the government in the past, there are some different points compared to private financial institutions.

Deposit limit

Japan Post Bank has a deposit limit that private financial institutions do not have. The deposit limit has been gradually increasing, and now the total amount is 26 million yen, which is 13 million yen for ordinary savings and 13 million yen for term savings.

Japan Post’s term savings

For fixed-rate deposits with a deposit period of less than three years, there are single-interest types, while 3, 4, and 5 years have half-year compound-type fixed-term savings.

Foreign currency-denominated financial instruments

All foreign currency-denominated financial instruments are related to exchange rates. Even if you can make a large profit in the foreign currency itself, its value may decrease when converted to Japanese yen.

Since Japan currently has low interest rates, foreign deposits and foreign bonds can be expected to have large interest rates, but it is necessary to pay attention to the exchange rates of the yen’s appreciation and depreciation of the yen, as well as the exchange rates in which financial institutions handle them.

Foreign currency deposits

Deposits made in foreign currencies such as the U.S. dollar, Australian dollar, and euro.

One of the attractions of foreign currency deposits is the goodness of interest rates. Because Japan is currently at ultra-low interest rates, the good interest rates in foreign countries stand out.

MMF denominated in foreign currency

What is Money Market Funds (MMF)?

MMF is an additional type of public and corporate bond investment trust that operates mainly in short-term financial products such as public and corporate bonds in Japan and overseas. Simply put, you can expect a higher interest rate than a term deposit, but in the worst case, it is like a deposit that may crack the main account (the money you put in will be reduced and returned).

MMF denominated in foreign currencies is less restricted than foreign currency deposits, and interest rates and exchange rates are often advantageous. The following are the procedural features of MMF denominated in foreign currency.

- It is necessary to open a foreign securities trading account.

- Foreign securities trading account management fee is not required for transactions denominated in foreign currencies only.

- The payment of cash is received the day after the application date.

- Foreign exchange gain is taxed separately, distribution is withholding tax

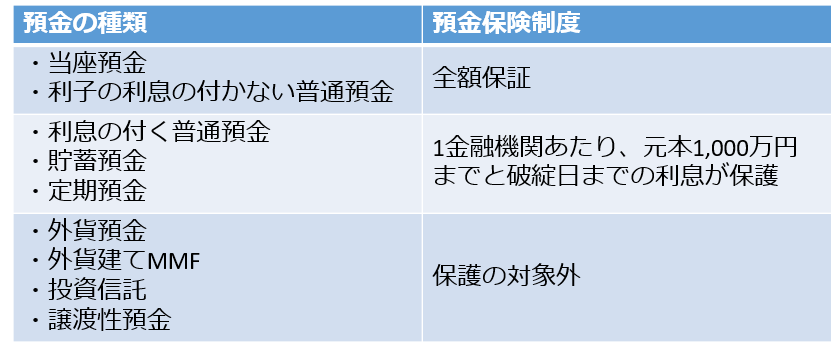

Deposit insurance

Money deposited with a financial institution is protected by the deposit insurance system even if the financial institution collapses. The scope and scope of the deposit depend on the type of deposit.

Savings without current accounts or interest (settlement deposits) are fully protected.

Savings and savings deposits with time deposits and interest are protected up to 10 million yen per financial institution and interest up to the date of failure.